Grahamian Value Week in Review ― March 5, 2021

“As Ben Graham noted in his classic, The Intelligent Investor, ‘It always seemed, and still seems, ridiculously simple to say that if one can acquire a diversified group of common stocks at a price less than the applicable net current assets alone — after deducting all prior claims, and counting as zero the fixed and other assets — the result should be quite satisfactory.’ Apparently, in today’s world of efficient markets, investors can still profit from Ben Graham’s sage advice.”

— Joel M. Greenblatt, Richard Pzena and Bruce L. Newberg (1981)

PART ONE.

WEEK IN REVIEW

PART TWO.

WEEKEND READING

PART THREE.

WEEKEND WATCHING

PART FOUR.

WEEKEND LISTENING

OVERVIEW —

No changes to the Grahamian Value Classic list.

We explore the early writings of Joel Greenblatt, Richard Pzena and Bruce L. Newberg.

We proudly announce the inaugural Grahamian Value Fireside Conversation.

I. WEEK IN REVIEW

This marks our twenty-first consecutive week with no new additions to the Grahamian Value Classic list of companies.

Join us for the inaugural Grahamian Value Fireside Conversation taking place on Thursday, March 11, 2021 at 7:00 PM Eastern Standard Time (UTC-5)— featuring Nicholas E. Radice; advanced registration (direct link) is required to participate.

II. “HOW THE SMALL INVESTOR CAN BEAT THE MARKET”

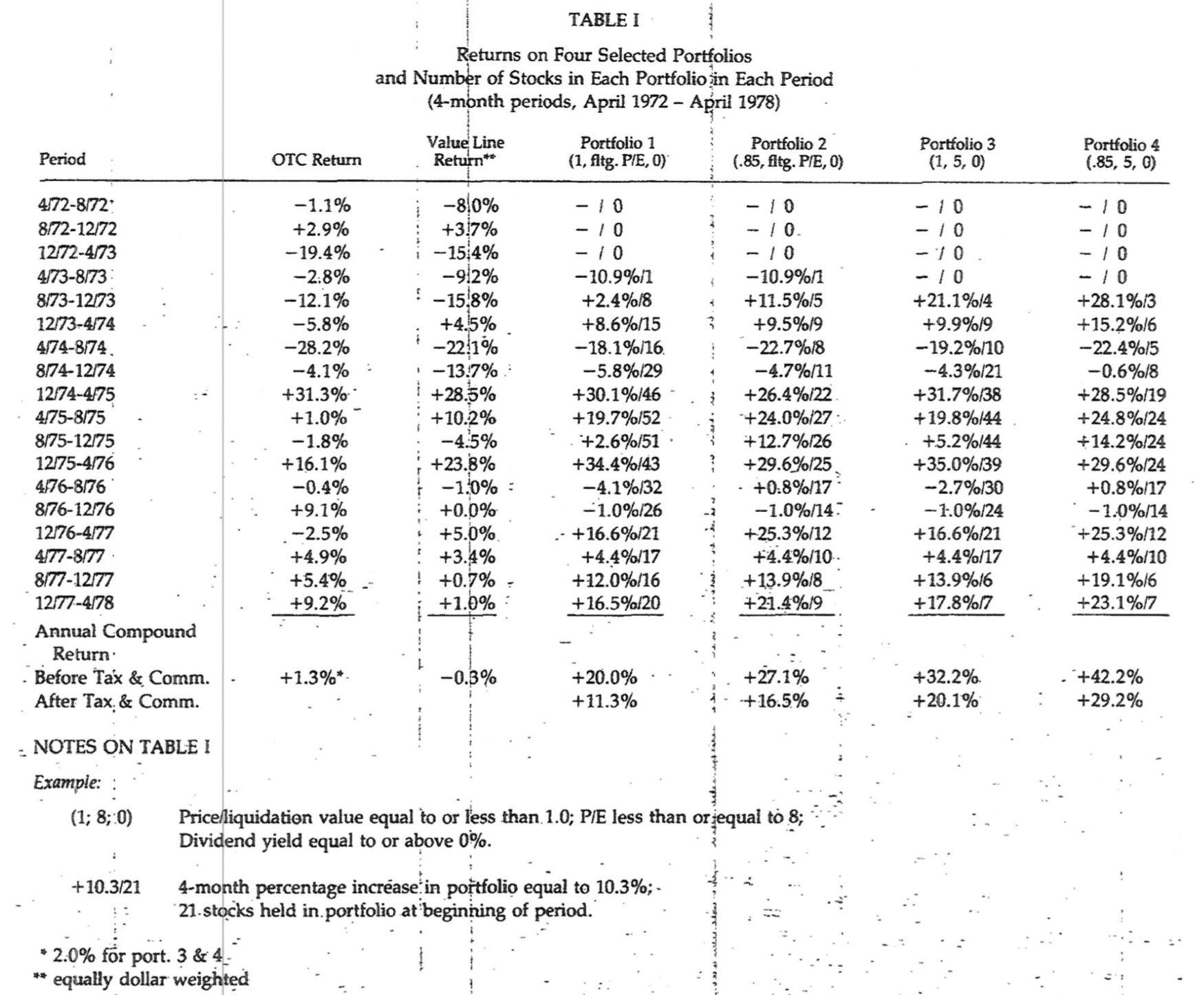

We remain most intrigued by Joel Greenblatt’s early writings as a graduate student at the University of Pennsylvania. Published in the Summer 1981 issue of Journal of Portfolio Management, Joel Greenblatt, Richard Pzena and Bruce L. Newberg studied “stocks that are selling below their liquidation value” in the period from April 1972 to April 1978.

The trio’s study “looked exclusively at three factors: (1) price in relation to liquidation value, (2) price/earnings ratio, and (3) dividend yield” — buying any stock that met the defined criteria, selling after a 100% gain or after two-years (whichever came first), while assuming an equal dollar-weighted amount invested in each stock in the portfolio.

Portfolio 1: Required a price no greater than liquidation value, an earnings yield at least twice that of the prevailing triple-A-rated bond yield, and had no dividend requirements.

During the 15 4-month periods our constraints dictated a position in the market, we averaged an annual compounded rate of return of 20.0% before dividends, commissions and taxes. The OTC index appreciated at an annual compounded rate of 1.5% during the same period.

Portfolio 2: Required a price no greater than 85% of liquidation value, an earnings yield at least twice that of the prevailing triple-A-rated bond yield, and had no dividend requirements.

After we limited the purchases in Portfolio 1 to stocks selling below 85% of liquidation value, the returns increased to a 27.1% annualized rate before dividends, commissions, and taxes (compared with the market's 1.3% annual performance). After taxes and commissions, this return approximated 16.5% annually.

Portfolio 3: Required a price no greater than liquidation value, a P/E ratio no greater than 5, and had no dividend requirements.

When we used a low constant P/E ratio coupled with a discount to liquidation value, our returns were significantly improved to a 32.3% annualized rate before dividends, commissions, and taxes. After taxes and commissions, our return falls to 20.1% per year, compared to the OTC market's return of 2.0% during the 14 periods when we had a position in the market.

Additionally, the study notes —

No stocks were purchased until August 1973 using the parameter of a PE below 5. The portfolio also entered the market closer to the trough and with more conservatively valued stocks. We outperformed the OTC index by 5% or more in 9 four-month periods, while we underperformed the market by 5% in only one period.

Portfolio 4: Required a price no greater than 85% of liquidation value, a P/E ratio no greater than 5, and had no dividend requirements.

Our most successful screen. It resulted in an annualized rate of over 42.2% before dividends, commissions and taxes. The result before dividend returns approximated 29.2% for the 14 periods studied, compared to the 2.0% annual returns of the OTC markets.

A word from the co-editors: Among several implications from the granular data, we note the absence of net-nets from mid-1972 thru mid-1973 (and subsequent proliferation).

As explored last week, we understand that Michael Burry owns a collection of Japanese public equities, several of which are traditional net-nets with strong individual histories of profitability.

Alternatively stated, Michael Burry’s selection of small and overlooked Japanese equities squarely fit within the parameters of the above 1981 study.

III. WEEKEND WATCHING

Courtesy of Yahoo Finance: Charlie Munger speaks at the Daily Journal Corporation Annual Meeting. (Streamed live on February 24, 2021)

Full Transcript — courtesy of Richard Lewis

Courtesy of Penn Graduate School of Education: Join us for a conversation with Donald E. Graham, chairman of the board of Graham Holdings Company (previously The Washington Post Company) and co-founder of TheDream.US; and Joel Greenblatt, W’79 WG’80, GSE Overseer, managing partner of Gotham Capital, and co-founder of Success Academy Charter Schools. They share their perspectives about some of today’s most pressing issues in education in a dialogue with Dean Pam Grossman. (Recorded on May 12, 2018)

IV. WEEKEND LISTENING

Courtesy of KindredCast: Dr. John Malone, the legendary businessman, philanthropist and conservationist, who serves as Chairman of Liberty Media, Liberty Broadband, and Liberty Global, sits down with Aryeh Bourkoff for a comprehensive discussion. The “cable cowboy” reflects back on an incredible career that has shaped the content and cable industries on a global scale. Dr. Malone also shares his thoughts on happiness in the midst of a pandemic, the state of play in the media and the frothy markets that we are seeing; he also shares his greatest hits and some very interesting misses throughout his career. (February 26, 2021 episode date)

ABOUT GRAHAMIAN VALUE

Founded in 2020, Grahamian Value is a open resource dedicated to the art of intelligent investing.

The co-editors of Grahamian Value, as of the date of this communication, may individually own shares of companies mentioned herein. The publishers do not receive compensation from the companies and people covered in Grahamian Value for such coverage. This communication is for informational purposes only. This is not intended to be investment advice. Seek a duly licensed professional for investment advice.