Grahamian Value Week in Review ― November 6, 2020

“Inaction and patience are almost always the wisest options for investors in the stock market.”

— Guy Spier, The Education of a Value Investor (2014)

PART ONE.

WEEK IN REVIEW

PART TWO.

FEATURED LOCAL INSIGHTS

PART THREE.

WEEKEND READING

PART FOUR.

WEEKEND LISTENING

PART FIVE.

IN TRIBUTE

In the past week —

No new businesses have been added to the Grahamian Value list of companies.

We’ve noticed interesting developments at five Grahamian Value listed companies.

BRIEF OVERVIEW —

As many readers will likely notice, this is our fourth consecutive week with no material change in the list of Grahamian Value companies.

We note the continued dislocation in energy, with the sector making up the largest proportion of companies on the Grahamian Value list.

I. WEEK IN REVIEW

Updated Financials: NOW Inc.

NOW Inc. reported financials for the quarter ending September 30 on their Form 10-Q filed November 4, 2020, reporting a GAAP loss of $22 million, or roughly negative $0.20 per share, and generating $59 million in cash from operations while spending $2 million on capital expenditures. Though this level of capital expenditure is extraordinarily depressed, it indicates relative flexibility of expenditures, such that NOW Inc. can make investments when it is opportune to.

NOW Inc.’s unadjusted net current asset value (per the co-editors’ calculations) is about $570 million or slightly above $5.20 per share, comprised of $325 million in cash and equivalents, $213 million in receivables, $318 million in inventories, $6 million in assets held-for-sale, and $16 million in prepaid expenses and other current assets; less $308 million in total liabilities, comprised primarily of accounts payable. NOW Inc. has no long-term debt and a very small ($28 million) operating lease liability.

We specifically note the exchange below from the company’s most recent quarterly conference call, held on November 4, 2020 (with emphasis added):

Sean Meakim, Senior Equity Research Analyst at J.P. Morgan:

…Are you able to give us a framework around kind of a trough peak versus normalized type of EBITDA margin going forward, relative to maybe what you were able to accomplish in the prior cycle?

David Cherechinsky, President and Chief Executive Officer of DistributionNOW:

Yes, so you want me to forecast an EBITDA target. I mean what I first want to do is get the business to breakeven. And ultimately, we’ve talked, historically, we’ve been in the 5% EBITDA range. We definitely want to get back to that level and higher. But first, we need to get to breakeven. So, we've seen our North American market decline by 80% since 2014. We’ve made significant restructures in the business. We’re kind of pursuing a fulfillment central migration where we’re moving our business to more of a centralized model. So getting to the right level of WSA [warehousing, selling and administrative expenses] in the business, forecasting the revenues, all of that has to come together to — before we start talking about what kind of EBITDA progression. But I would tell you, 5% is a minimum starting point, and we need to get to breakeven first. We believe we’ll get to breakeven in the first half of 2021.

…After the worst oilfield industry since the Great Depression, we’ve done heroic work in this company to get to where we're at right now. So first, we need to get to breakeven. We have a plan to do that. And then in the spirit of your question, then we need to get to meaningful EBITDA numbers. And 5% would be a base — and above that would be where we need to go as we as we buy companies, as we divest parts of our business that aren’t profitable and as we high grade all those things that work and don't work in our business.

Two additional notes from the co-editors —

This March 18, 2015 write up by “MJS27” on Value Investors Club is a very interesting read, with emphasis added to the following excerpt:

Generally speaking, distribution is a great business. Once your two-sided network is built out, your cap-ex is almost nothing. How much does it cost to keep the lights on in a warehouse? Almost nothing. In NOW Inc.’s case they believe maintenance capital expenditure is around $10-15 million [as of 2015].

The build out is the hard part because scale matters for distributors. The end users want to deal with a distributor who has a large supplier network and thus a wide assortment of SKUs for convenience sake, and the products are essentially commodities, so price matters. Low prices of course come from a wide network of end users, so that you can buy in bulk from your suppliers and thus get volume discounts. Fixed costs such as home office etc. benefit from operational leverage at the top level, and fixed costs such as storage and delivery benefit from operational leverage at the regional level, further contributing to pricing advantages. The bigger the two-sided network gets, the deeper the moat becomes as competitors are unable to compete on price. The worse the environment gets, the better it is for the low cost providers because end users push harder and harder for price concessions, and the low cost providers can withstand more pain and thus lower prices than the competition. This leads to market share gain. Market share gain reinforces the cycle. Overtime, the big boys have more money to throw around, which means they can spend more money and time integrating themselves with their customers through on site locations and coordinated IT systems, which raises switching costs.

Importantly, the bad times are when the end users most appreciate the fact that they have a distributor rather than sourcing their own supplies, because using a distributor essentially lets them keep their inventory off balance sheet which frees up cash from working capital for the lean times. At the same time, distributors also benefit from working capital release during the bad times because they simply do not replenish inventory as it is consumed by their end users.

The oil field distribution industry is extremely fragmented, with NOW Inc. and MRC Global Inc. together representing about 50% of the business, and sub-scale competitors representing the other 50%. MRC Global Inc. is bigger than NOW Inc., but they currently have limited liquidity due to an already 4x levered balance sheet [as of 2015]. That means that the competition is either under-scaled or over-levered, leaving NOW Inc. as the most capable consolidator in the space as others get squeezed out.

Slide 5 adds further context on DistributionNOW's strategy to unlock value for shareholders.

Courtesy of TIKR.com (which we use, love and wholeheartedly recommend!) —

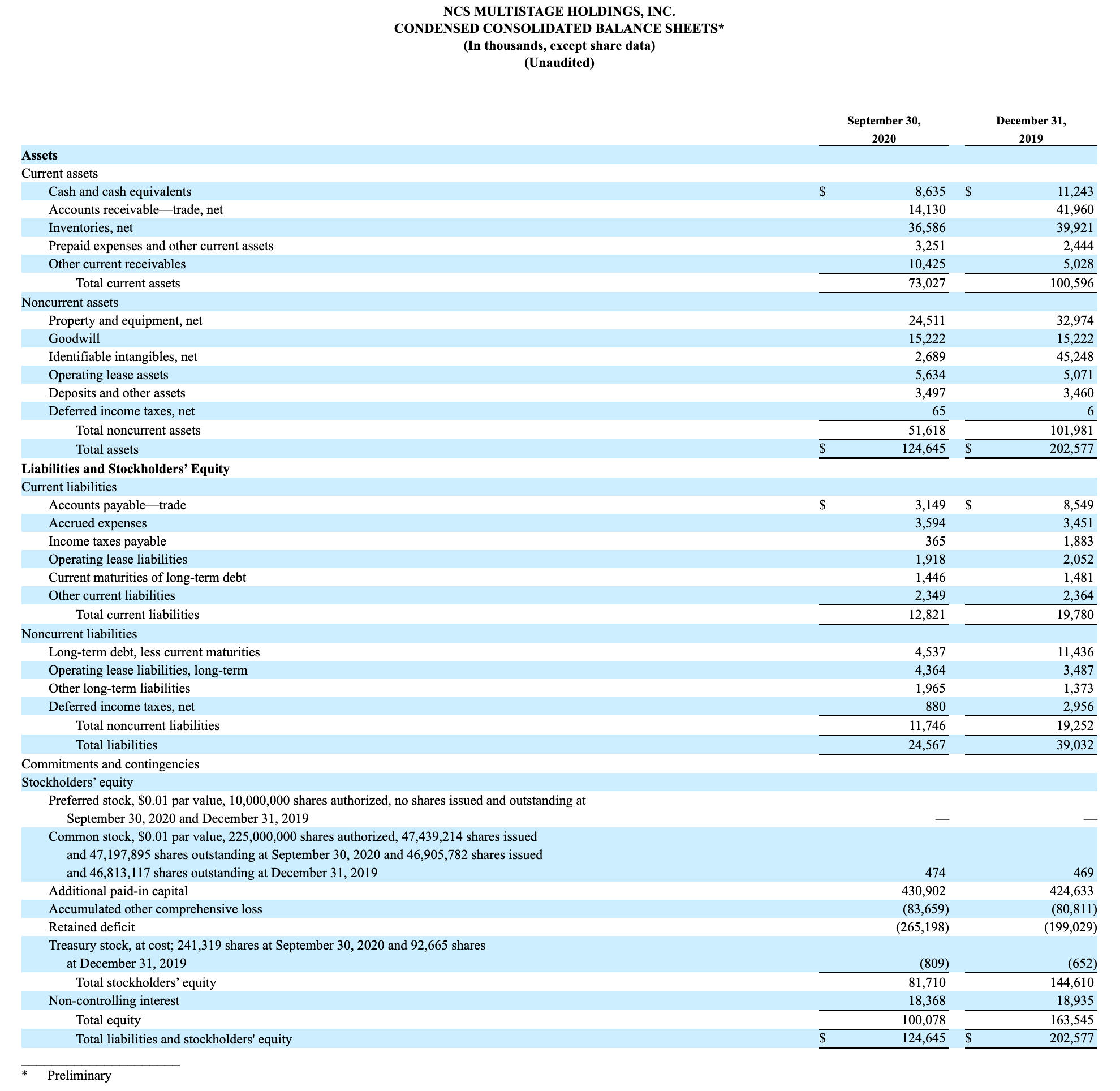

Updated Financials: NCS Multistage Holdings, Inc.

NCS Multistage Holdings, Inc. reported financials for the quarter ending September 30 on Form 8-K filed on November 4, 2020, with a net loss just under $6 million or about negative $0.12 per share. At the quarter end, NCS Multistage had $8.6 million in cash and equivalents and $4.2 million in undrawn senior secured credit facility capacity. The company additionally reported Adjusted EBITDA of negative $2.1 million, with adjustments consisting of the non-cash or non-recurring (but nonetheless real) expenses of $1.6 million in stock-based compensation, $1.2 million in professional fees, and $844,000 in severance costs.

Per the above 8-K, NCS Multistage had an unadjusted net current asset value of just under $49 million, or slightly over $1.00 per share — comprised of $8.6 million in cash and equivalents, $24.5 million in receivables, $36.5 million in inventory, and $3.2 million in other current assets; less $24.6 million in total liabilities, largely in $3.1 million of payables, $3.59 million of accrued expenses, and non-current, long-term debt and lease obligations of $8.9 million.

NCS Multistage is “committed to a continued NASDAQ listing” and the board of directors recently approved a measure to conduct a 1-for-20 reverse split to regain compliance with NASDAQ minimum bid requirements. We also note that Advent International Corporation beneficially holds 29,568,536 shares of NCS Multistage’s common stock, or approximately 62.6% of shares outstanding.

Updated Financials: Gulf Island Fabrication, Inc.

Gulf Island Fabrication filed their Form 10-Q with the SEC on November 3, 2020 reporting financials for the quarter ending September 30. Gulf Island notably reported a significantly larger negative gross profit (negative $7.8 million, compared to negative $1.7 million for the prior quarter) and using $3.5 million in cash for operating activities.

Unadjusted net current asset value at the quarter end was $52.1 million, or $3.40 per share — comprised of $43.8 million of cash and equivalents, just under $20 million of short-term investments, $24.4 million of receivables, $72.3 million of contract assets, $2.3 million of prepaid expenses, $2.5 million of inventory, and $7.6 million of assets held for sale; less $120.9 million in total liabilities, consisting mostly of accounts payable.

Updated Financials: Newpark Resources, Inc.

Newpark Resources, Inc. filed Form 10-Q on November 4, 2020, reporting a quarterly net loss of $23.87 million, or negative $0.26 per share. Gross margins were negative, but the company generated $40.29 million in operating cash flow and $25.68 million in free cash flow, or roughly one-third its market cap in a single quarter. This theme of negative gross margins, depressed capital expenditure, and positive operating cash flow seems common across the energy names among GV | US companies.

From an asset value perspective, Newpark Resources had $94.9 million in unadjusted net current assets, or $0.88 per share, comprised of $24 million in cash and equivalents, $127.96 million in receivables, $159.57 million in inventories, and $17.33 million in prepaid expenses and other current assets; less $233.96 million in total liabilities, mostly in long-term debt and leases, as well as short-term payables and accrued expenses.

CFO Resignation: Rubicon Technology, Inc

On November 3, 2020, Mathew Rich gave Rubicon Technology, Inc. (the “Company”) notice that due to certain health issues, he is going on disability and that he can longer serve as the Company’s Chief Financial Officer effective immediately. The Company’s Chief Executive Officer, Timothy Brog, will be the Acting Chief Financial Officer, until Mr. Rich’s replacement has been hired. The Company has begun a search for a new Chief Financial Officer and will announce such person as soon as one has been hired.

Source: Form 8-K, filed November 3, 2020.

II. FEATURED LOCAL INSIGHTS

The piece below is republished with the permission of WarwickB (twitter), who runs OceaniaValue.com — an online resource the co-editors particularly enjoy. Emphasis to the following text is added by the co-editors. Guest insights (such as WarwickB’s) and further discussion of investment ideas are always welcomed; we can be reached at GrahamianValue@gmail.com.

Important Message for All Readers: While the co-editors admire the above showcased thought leader, all opinions expressed are subject to error and the material below is intended for educational purposes only. The public equities explored below are thinly-traded and listed on local exchanges, subject to local regulations and norms. Particular prudence is warranted, personal diligence is always strongly advised.Net-Nets: Opportunities in Malaysia

It’s a lot easier to find net-nets in Malaysia than in my home market (Australia) but nowhere near as easy as it is in Japan… I know of around a dozen Malaysian net-nets — not enough of these are of sufficient quality to make a diversified basket…

Why does Malaysia have net-nets? I think in recent times the answer in any country is the same three reasons:

There is a supply of illiquid, overcapitalized companies which often have the means but not the will to immediately return funds to shareholders through aggressive buybacks or special dividends.

There is a dearth of buyers willing to take the chance that a payout can somehow be obtained by buying the stock and waiting for a happy accident.

There is a lack of a powerful owner intent on breaking the deadlock. I.e. no activist funds or the net-nets are controlled companies.

…In most cases the companies are controlled. Malaysia’s stock market is tiny and most foreign brokers don’t cover it. It’s highly unlikely that foreign investors will come in and start buying these companies.

Malaysian net-nets are different than Japanese ones. Over-capitalization in Malaysia tends to come from a lack of perceived opportunities to deploy cash, rather than a desire to provide stability for employees in the event of an economic downturn… Malaysian net-nets tend not to have a previous, much higher stock price. Sadly, they are much less volatile than Japanese net-nets.

Given that we have a bunch of mostly controlled companies with no clear path to a payout most people would say these stocks are dead money. Why on earth do I buy them?

…I might not buy them if I could find a few more higher yielding stocks which I’m confident enough to hold concentrated positions in — I buy them because:

Many of them provide a higher dividend yield than can be obtained from cash or government bonds.

Many of them are durable companies that can preserve or grow their excess capital for several years through ongoing operations.

Whilst I have no evidence to believe there is an imminent catalyst for most of them, I’d prefer to put a portion of my portfolio into a basket of net-nets and see if I get lucky than keep that portion in cash or in higher yielding (but lower conviction) ideas.

Without an activist fund on the horizon, how might I get lucky? One way would be for management to aggressively reinvest in a productive asset that would increase income and hence increase the dividend or rate of growth in NTA. There is evidence to suggest this may happen with JcbNext and Kluang.

Another way would be for the controlling owner to take the company private. This happened recently with a restaurant net-net which I passed on last year, Oversea Enterprise Bhd (KLSE:OVERSEA). Oversea had been loss-making for six years and was trading at around half of NAV. The managing director bought an additional 62% of the company’s shares off-market which triggered a mandatory takeover offer for the remainder of the company at around 5 times the previous share price.

Oversea’s premium to VWAP is an extreme example — most going private transactions aren’t as profitable. Of the 30 similar transactions I can find which have taken place in Malaysia since 2006, most paid around a 20 to 30% premium to the 6-month VWAP. I didn’t buy Oversea because it was loss-making and I wouldn’t buy it if I had my time again. But it does illustrate one thing — the returns from this type of portfolio are not normally distributed. If you had bought Oversea as part of an equal-weight basket of ten ‘dead money’ net-nets, you could have held the basket for four years and earned better than 10% CAGR if the other stocks collectively returned zero.

Below is a list of the net-nets that I think are not totally dreadful at the time of writing… I find that the most useful sources for financial data and annual reports are the company websites. These usually have a 5-year financial summary and they tend to have the annual reports for download as a single file, which is better than the multiple files on the Bursa Malaysia website. It’s also worth reading the mandatory summary of AGM questions and responses on each company’s website, a practice I wish was common in other countries.

JcbNext Bhd (KLSE:JCBNEXT)

JcbNext holds the assets of Malaysia’s leading job portal, minus the actual job portal business which was sold in 2014. The company’s main assets are shares in 104 Corporation (TW:3130), Lion Rock Group (HK:1127) and a handful of other listed companies. There is also a large cash balance which management intend to deploy when they can find a suitable opportunity. JcbNext is controlled by a self-professed Buffett-style investor. They pay a dividend and have been slowly but consistently buying back shares recently at a large discount to tangible book.

Kluang Rubber Company (Malaya) Bhd (KLSE:KLUANG)

Kluang is a rubber plantation company from the 1920s which has cross-holdings with two other consolidated KLSE listed entities (SBAGAN and KUCHAI). Assets include 1% of large life insurer Great Eastern (SGX:G07), properties in London and Singapore and a large cash holding. The controlling family run a value fund in Singapore and they have been pretty clear about waiting (and waiting) for the right opportunity to deploy their cash. Have a look at www.cam.com.sg from pre-2011 on archive.org for an insight into their thinking. There’s no chance of a liquidation or large special dividend here but the share price roughly tracks the increase in tangible book and previous bonus issues carried out to maintain compliance with public float rules have caused the share price to increase. Pays a small dividend and occasionally buys back small parcels of stock.

Insas Bhd (KLSE:INSAS)

Insas is a stockbroking/M&A firm that also owns a car rental business, a large share of KLSE tech darling INARI and dabbles in property development like most other KLSE listed companies. The company has a large cash balance but care needs to be taken as much of Insas’s cash and assets are pledged as collateral for their brokerage business. At the time of writing Insas recently announced an issue of renounceable preference shares with attached warrants which looks interesting as a special situation.

FACB Industries Incorporated Bhd (KLSE:FACBIND)

FACB is a mattress manufacturer which sells into the Malaysian and PRC markets and also owns a power generation operation in the PRC. Current assets consist largely of a large cash holding (net of any CNY amounts) and KLSE-listed shares. Management owns 30% of the company. Pays a modest dividend.

Dutaland Bhd (KLSE:DUTALND)

Dutaland is best known for the incomplete high-rise tower next to the Renaissance Hotel in Kuala Lumpur. Last time I saw this structure the lower floors were slowly returning to nature but the company intends to restart construction despite the project being halted since the Asian crisis in 1998. Dutaland has a few other active property development projects and a large cash balance as a result of the sale of their palm oil plantation division. Management owns 55% of the company and is buying back stock. The bought-back shares are held in treasury so I wouldn’t be surprised to see them re-issued to fund the high-rise project if they can’t find a JV partner.

Farlim Group (M) Bhd (KLSE:FARLIM)

Farlim is a property developer which specializes in township developments near Penang. The company hasn’t paid a dividend since 2016 but has been repurchasing (but not cancelling) shares. Management owns 43% of the float. Most of the liquid assets are in KLSE listed shares and money management funds.

Lion Posim Bhd (KLSE: LIONPSIM)

Lion is a construction materials and lubricants company which is an affiliate of the group of companies which controls the Parkson department chain franchise in the region. The company has repurchased shares in the past but pays no dividend. Large impairment charges in 2016 and the preceding years led to large losses at the net income line but the operating profit has been positive for at least 10 years.

Co-Editor’s note: the author can be reached directly at oceaniavalue@gmail.com and welcomes Grahamian Value reader feedback.

III. WEEKEND READING

Investment Strategy Commentary from Northern Trust Global Asset Allocation —

Value Stocks: Trapped or Spring-Loaded? (September 24, 2020): “…we sorted Russell 1000 Index companies by their five-year growth expectations, bucketed into quintiles… the top quintile (highest growth expectation) stocks only beat those lofty expectations 38% of the time. Meanwhile, the fifth quintile stocks beat relatively low expectations 54% of the time. Notably, this study looks at the 2013-2019 period, wherein many growth (specifically tech) stocks’ earnings potential has been under-appreciated.”

IV. WEEKEND WATCHING

Courtesy of Yet Another Value Channel, hosted by Andrew Walker (twitter): Michael Melby, founder and portfolio manager of Gate City Capital in Chicago, discusses his professional background and investment into AMREP Corporation. Gate City Capital is a 17.9% owner of AMREP Corporation. (Recorded November 2020)

Courtesy of Talks at Google: Guy Spier, founder and portfolio manager of Aquamarine Capital in Zürich, explores “The Education of a Value Investor: My Transformative Quest for Wealth, Wisdom, and Enlightenment.” (Recorded September 2014)

V. IN TRIBUTE

Courtesy of Ivey Business School: Walter Schloss was the Founder of Walter & Edwin Schloss Associates in New York. (Recorded February 12, 2008)

Courtesy of Ivey Business School: Irving Kahn was the Chairman of Kahn Brothers & Company Inc. in New York. (Recorded March 7, 2005)

Courtesy of Ivey Business School: Peter Cundill was the Principal of The Cundill Group in Vancouver, British Columbia. (Recorded March 28, 2005)

ABOUT GRAHAMIAN VALUE

Founded in 2020, Grahamian Value is a open resource dedicated to the art of intelligent investing.

The co-editors of Grahamian Value, as of the date of this communication, may individually own shares of companies mentioned herein. The publishers do not receive compensation from the companies and people covered in Grahamian Value for such coverage. This communication is for informational purposes only. This is not intended to be investment advice. Seek a duly licensed professional for investment advice.